Authored by Rick Devine - Follow Rick on Talentsky

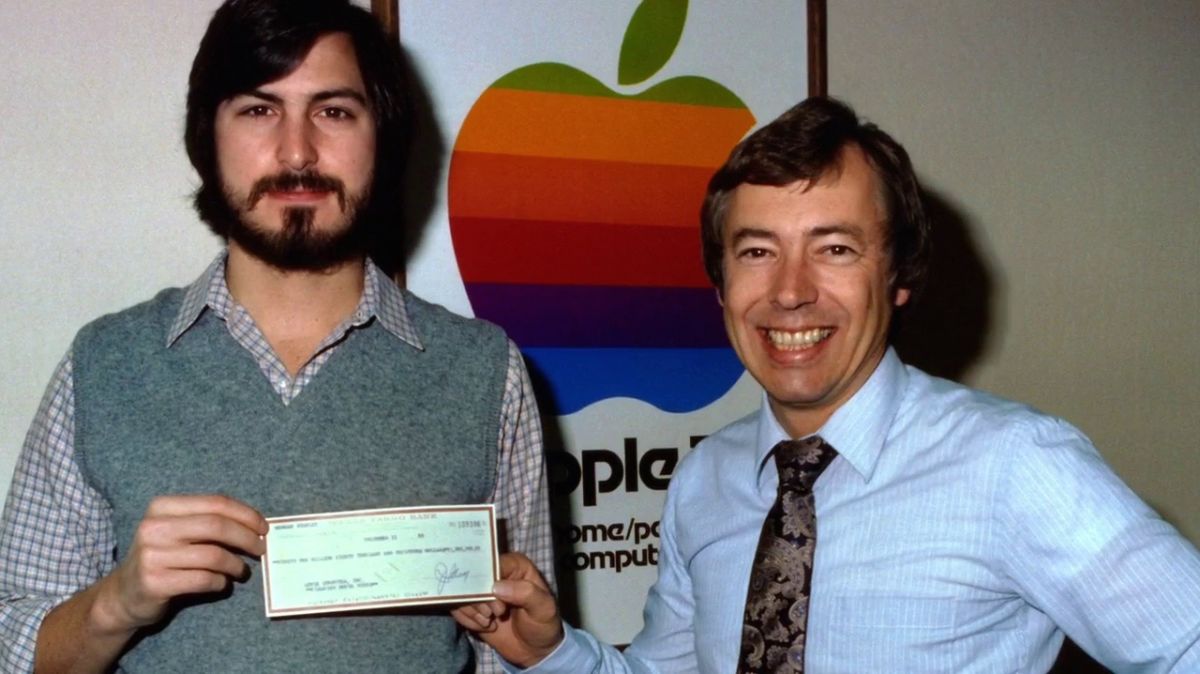

It was the late 1970s and Silicon Valley was still an infant. Dave Packard and Bill Hewlett laid the groundwork in the 60s, which inspired a young Steve Jobs. Then, then the semiconductor industry followed – including Fairchild Semiconductor and a start-up of rebels who left to found Intel. One of the founders of Intel was Mike (A.C.) Markkula, who later ran into two young kids (both named Steve), who had a vision for making computers for everyone. Mike decided to write the first check to their company, Apple Computer, Inc.

What did Mike see in Steve Jobs and Steve Wozniak? Did he see a detailed five-year plan? No. Did Mike raise money from pension funds to then invest in Apple? No.

What Mike saw was a game-changing idea with passionate founders like himself. Mike knew how hard it is to change an industry and build something from scratch. He backed Apple with his personal money and his commitment to be a supportive partner. Mike Markkula was one of the original Silicon Valley venture capitalists. His backing and support of Apple, Steve Jobs and Steve Wozniak helped make their dream a reality.

Then, there’s the story of Don Lucas and Larry Ellison. In the late 1970s, Don was working in a small office on 3000 Sand Hill Road, where most venture investors were located. One late night, he bumped into Larry Ellison in the parking lot. Larry and Bob Miner had started a consulting company called Relational Software, Inc. to implement a database project for the CIA. Don saw the hard work and dedication of Larry Ellison and wrote a check – with his personal money – and invested in RSI, which later changed its name to Oracle Corporation. There was no forecast, no business plan – just an investor who saw in Larry Ellison what makes all great success stories: vision, hard work and perseverance.

So, what happened? How did the Silicon Valley venture capital industry change? In the early 1980s, venture capital became a category allocation for large institutional investors and VCs became managers of another manager’s capital. The typical structure was “2/20.” That is, a venture capital firm would charge a management fee of two percent every year based upon the capital commitment from their limited partners. If the fund was $100m, the firm would charge $2m in fees. If the fund was $1b, the firm would charge $20m in fees. Keep in mind, venture firms do not have a lot of people, leading to well over $1m salaries for venture partners. On top of the management fee, the venture firm would charge a “carried interest” of 20% on gains. For example, if a venture fund returned $500m of gain on $100m of investment, they would earn $100m in equity value. If a $1b fund simply doubled, that’s $200m for the partners while they are earning $20m for their effort. Do the math: this is a very lucrative business.

So, what’s the problem? There is nothing wrong with a capital manager making money. However, venture capital means innovation capital and innovation requires patience. Most people do not realize it can take seven to ten years for a big idea to become reality, and another ten years to mature. The first ten years of a start-up are dog years, filled with trial, failure, more trial, more failure, etc. Only the commitment of a founder can endure this type of stress. The founder needs a capital source that will go long – and reap the return associated with a big idea becoming a category leader. Much has been said about Steve Jobs, but there is one attribute I admired most: how he was able to endure during the tough times.

The venture capital industry today is not structured to be patient. As venture firms raise more and more capital, and increase their fee income, they make promises to their investors to deliver a return within the ten year life of the fund. With this time frame as a pressure, many venture capital investors give up too early, or panic when they see problems. Meanwhile, some of the greatest success stories in recent times did not receive venture capital backing, including Salesforce.

Marc Benioff had a bold vision and patiently waited for the world to catch up. In the early days, Salesforce sold three to five user licenses via credit card, with an inside sales organization they called “corporate sales.” They created a culture around cloud computing, won the confidence of the industry, and ultimately were able to sell bigger deals to the enterprise. I recruited leaders for Salesforce when the company had fewer than 100 people in San Francisco. I would tell candidates, “Marc is a visionary and if you stick with him, he will build the next Oracle.” Some of these candidates – like many in the current venture capital industry – missed a great opportunity to partner with one of the greatest tech entrepreneurs of our time.

Years ago, when I started Talentsky, I told my family I was going long – committing the next 20 years of my professional life to the creation of a new platform that would help the American workforce understand the value of their skills, discover how they compare to careers of interest, and connect to education needed for a better future. I told them I would invest all the money we had, borrow more if needed, and raise capital from real venture investors – not VC firms, but people who believe in what we are doing and backed my vision and unwavering commitment to this challenge. Today, we have raised over $40m without a single venture capital firm, but over 200 venture capitalists.

Go Talentsky!